Table of Contents

Many savers across the UK are unaware that they could be earning interest on their savings completely tax-free. With the right combination of allowances and careful planning, a significant portion of savings income can remain untaxed.

In this guide, we break down how much interest you can earn tax free, which allowances apply to different income levels, and how to manage your savings efficiently. Understanding how tax-free interest works could help you keep more of your hard-earned money.

What Is the Personal Savings Allowance and How Does It Work?

The Personal Savings Allowance (PSA) is a tax-free threshold for interest earned on savings. It allows basic rate taxpayers to earn up to £1,000 in interest each year without paying tax. For higher rate taxpayers, the allowance is £500, and for additional rate taxpayers, there is no allowance.

This allowance applies to a wide range of interest income, including from bank accounts, credit unions, building societies, corporate bonds, and more.

- Basic rate (20%) taxpayers: £1,000 PSA

- Higher rate (40%) taxpayers: £500 PSA

- Additional rate (45%) taxpayers: £0 PSA

The PSA is calculated per tax year (6 April to 5 April) and depends on your total income, including wages, pensions, and savings interest.

What Counts as Savings Interest Under UK Tax Rules?

Savings interest refers to the money you earn from depositing funds into savings products. Different types of income qualify under the tax rules for savings.

Some common sources of taxable savings interest include:

| Source of Interest | Is It Tax-Free Under PSA? |

| Bank savings accounts | Yes |

| Credit union accounts | Yes |

| Fixed-rate bonds | Yes |

| Government and corporate bonds | Yes |

| Peer-to-peer lending platforms | Yes |

| Unit trusts and open-ended investment companies (OEICs) | Yes (interest only) |

| Dividend income from shares | No |

| Individual Savings Accounts (ISAs) | Exempt, not counted in PSA |

ISAs remain outside of PSA considerations as they are tax-exempt by nature. Dividend income is not included in the PSA; it falls under the separate Dividend Allowance.

Do You Have to Pay Tax on Interest from a Savings Account?

Whether or not you pay tax on your savings account interest depends on how much you earn from other income sources and how much interest you generate. If your total taxable income is low enough, you may not need to pay any tax at all.

Most savers benefit from at least the Personal Savings Allowance, which shields £500 to £1,000 of interest from tax depending on your income level. The interest is paid gross, and HMRC tracks it via reports from banks.

How Do Income Tax Bands Affect Tax-Free Savings Interest?

Your income tax band plays a vital role in determining how much savings interest you can earn tax-free. The higher your income, the lower your PSA becomes, and additional allowances may no longer apply.

Basic Rate Taxpayers

If you pay 20% income tax, you can earn up to £1,000 in interest tax-free. This group forms the majority of UK taxpayers and includes those earning between £12,571 and £50,270 per year.

Higher Rate Taxpayers

If you pay 40% tax, your PSA drops to £500 annually. Higher earners must monitor their savings more closely to avoid unexpected tax charges.

Additional Rate Taxpayers

Those earning above £125,140 get no PSA. Every pound of interest earned is taxable, so using tax-efficient wrappers like ISAs becomes crucial.

These thresholds help HMRC ensure that tax-free interest benefits low and middle-income savers the most.

What Is the Tax-Free Savings Limit for Basic Rate Taxpayers?

Basic rate taxpayers benefit from the most generous PSA of £1,000. This means you can earn up to £1,000 in interest from eligible savings before any tax is due.

Assuming an average savings account rate of 5% AER, you’d need approximately £20,000 saved to reach this threshold.

- PSA: £1,000

- Typical savings needed to reach PSA at 5% AER: £20,000

- Interest above this amount is taxed at 20%

This threshold applies regardless of whether the interest is earned monthly or annually, provided it falls within the same tax year.

How Much Interest Can Higher Rate Taxpayers Earn Without Paying Tax?

Higher rate taxpayers can earn £500 in savings interest each year without paying tax, thanks to the reduced PSA. Once exceeded, any interest is taxed at 40%. The savings amount needed to hit this PSA varies based on interest rates.

| Account Type (AER) | Savings Needed to Hit £500 PSA |

| Easy access (5%) | £10,000 |

| Fixed-term savings (4.5%) | £11,111 |

Higher earners are encouraged to monitor both their salary and investment income to avoid creeping into higher tax brackets that reduce or eliminate allowances.

Are ISAs Still the Best Way to Earn Tax-Free Interest in the UK?

ISAs remain one of the most reliable methods for earning tax-free interest, especially as interest rates rise and PSAs are exceeded more easily.

The annual ISA allowance for 2025/26 is £20,000. Any interest, dividends, or capital gains earned within an ISA do not count toward your PSA and are completely tax-free.

For savers close to or above their PSA, shifting funds into an ISA offers protection from future tax bills. Even if rates fall, having savings in a tax-free wrapper is a safe long-term strategy.

Can You Combine ISAs and Personal Savings Allowance for Maximum Benefit?

Yes, combining ISAs with your PSA can help you legally avoid tax on more savings interest. Since ISAs are outside the PSA framework, they don’t use up your allowance.

To maximise tax efficiency:

- Use your full £20,000 ISA allowance

- Keep additional savings in high-interest accounts up to your PSA limit

- Monitor total interest across all accounts

This combined strategy ensures you’re getting the most from both systems without breaching thresholds that trigger tax.

What Types of Savings Accounts Offer the Highest Tax-Free Interest?

Choosing the right type of account is key to maximising your tax-free interest earnings. The type of account, interest rate, and payout frequency all influence your PSA usage.

Top options include:

- Easy-access accounts: Offer flexibility and competitive rates

- Regular savers: Fixed monthly contributions with higher rates

- Fixed-rate bonds: Lock funds for a set term for higher returns

- Cash ISAs: Protect interest from tax altogether

Some current rates on high-interest accounts can reach up to 5% AER. At that rate, even basic-rate taxpayers may reach their £1,000 PSA quickly, especially if savings are left to compound over time.

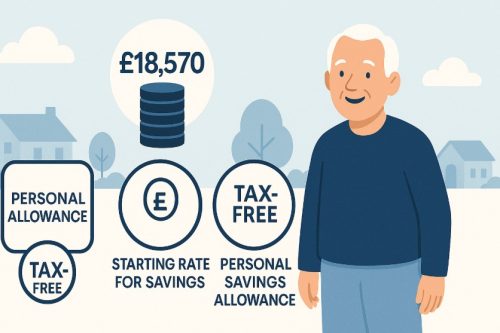

How Can Non-Taxpayers Maximise Their Tax-Free Savings in the UK?

Non-taxpayers, typically those earning below £12,570 annually, can combine several allowances to maximise tax-free interest. This includes the Personal Allowance, Starting Rate for Savings, and PSA.

| Income Type | Tax-Free Interest Potential |

| Personal Allowance | £12,570 income tax-free |

| Starting Rate for Savings | Up to £5,000 |

| Personal Savings Allowance | Up to £1,000 |

| Total (if fully eligible) | £18,570 |

This makes it possible for low-income individuals to earn substantial interest without paying tax, particularly if they don’t use their Personal Allowance for wages or pensions.

What Happens If You Exceed the Tax-Free Interest Threshold?

If your total savings interest goes beyond your PSA, you’ll need to pay tax on the excess. How this is handled depends on your employment status and tax arrangements.

- Employed or receiving a pension: HMRC adjusts your tax code

- Self-employed or with high savings income: Use Self Assessment to report interest

- Not employed and no pension: Banks report to HMRC; you’ll receive a tax notice

Other important points:

- You must pay tax at your usual income tax rate

- Overpayments can be reclaimed within four years

- If you go over the threshold and aren’t contacted, it’s your responsibility to report it

Staying within the limits or planning accordingly can help you manage your finances more effectively and prevent unexpected tax bills in the future.

Conclusion

Understanding how much interest you can earn tax free in the UK can significantly impact your savings strategy.

By making full use of the Personal Savings Allowance, Starting Rate for Savings, and tax-free accounts like ISAs, most people can legally avoid paying tax on their savings interest.

Keeping track of your income, interest earnings, and account types helps you stay compliant while making your money work harder. Savvy savers should regularly review their accounts and adjust their plans as interest rates and tax bands evolve.

Frequently Asked Questions

Is there a deadline to claim back overpaid savings tax?

Yes, you must reclaim overpaid tax within four years from the end of the relevant tax year.

Can I use my personal savings allowance on foreign interest?

Interest from foreign accounts is not always covered under PSA and may be taxed separately.

Do children’s savings accounts have tax-free interest?

Yes, but if a parent gifts the money and interest exceeds £100, it may be taxable under their name.

Will my savings interest push me into a higher tax band?

Yes, interest is part of your total income and could tip you into the next tax band.

What happens to savings interest in a trust or fund?

Trust-held savings follow different rules and often don’t qualify for PSA allowances.

How do Scottish taxpayers claim PSA allowances?

Although income tax bands differ in Scotland, the PSA uses UK-wide thresholds.

Is peer-to-peer lending interest also tax-free under PSA?

Yes, peer-to-peer lending interest qualifies under the PSA if within the set limits.

Also Read: