Table of Contents

If you are wondering how much savings you can have on ESA Support Group, the answer depends on which type of ESA you receive.

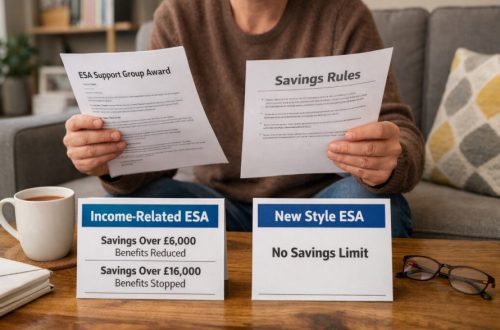

If you get income-related ESA, savings of up to £6,000 do not affect your payments. Savings between £6,000 and £16,000 reduce your ESA, while savings of £16,000 or more usually mean you are no longer entitled to income-related ESA.

However, if you receive New Style ESA or contribution-based ESA, your savings do not affect your claim at all.

Key points:

- Up to £6,000 in savings: no effect on income-related ESA

- Between £6,000 and £16,000: ESA is reduced

- £16,000 or more: income-related ESA usually stops

- New Style ESA is not affected by savings

- Your partner’s savings may also count

What Is the Savings Limit for ESA Support Group?

The savings limit for ESA Support Group depends on the type of ESA you receive, not the Support Group itself. Income-related ESA is means-tested, so your savings directly affect your eligibility, while New Style and contribution-based ESA are not affected by savings.

Key Highlights:

- Up to £6,000: No impact on income-related ESA

- £6,000–£16,000: Payments are reduced

- £16,000+: Usually no longer eligible for income-related ESA

- New Style ESA: No savings limit

- Contribution-based ESA: No savings limit

“For claimants on income-related ESA, capital over £6,000 affects entitlement, but New Style ESA is not means-tested,” a DWP spokesperson explained.

ESA Savings Rules Overview

| Type of ESA | Savings Limit | Effect of Savings |

| Income-related ESA | £6,000 before reduction | Reduced up to £16,000, then stops |

| New Style ESA | No limit | No effect on payments |

| Contribution-based ESA | No limit | No effect on payments |

Many claimants are unsure which ESA type they receive, so checking your claim details is essential to understand how savings affect your payments.

Does Being in the ESA Support Group Change the Savings Rules?

Being in the Support Group means the DWP has decided that your illness or disability severely limits your ability to work. It can increase the amount of ESA you receive, but it does not remove the savings rules.

If you are in the Support Group and receive income-related ESA, you may get up to £145.90 per week, plus extra premiums such as the enhanced disability premium. However, the DWP still checks how much money you have in savings.

Why the Support Group Does Not Override the Capital Rules?

The Support Group only affects your work requirements and the amount of ESA you receive. It does not create a separate entitlement rule for savings.

For example:

- A claimant in the Support Group on income-related ESA with £5,000 savings will receive their full ESA.

- A claimant in the Support Group on income-related ESA with £10,000 savings will have their ESA reduced.

- A claimant in the Support Group on New Style ESA with £20,000 savings can still receive full ESA.

How the DWP Decides Which Savings Rules Apply?

The DWP first checks what type of ESA you receive. If your award letter refers to “income-related ESA”, the savings limits apply. If your letter refers to “New Style ESA” or “contribution-based ESA”, your savings are ignored.

You can usually check this by looking at the most recent ESA letter sent to you or by contacting the DWP directly.

What Happens if You Receive Both Types of ESA?

Some people receive both contribution-based ESA and a small income-related top-up. In this situation, only the income-related part is affected by savings.

For instance, if you receive contribution-based ESA plus an income-related premium, having more than £6,000 in savings may reduce the extra income-related element, but your contribution-based payment can continue.

How Much Savings Can You Have on Income-Related ESA?

Income-related ESA has three main savings thresholds. These limits apply to the combined savings of you and your partner if you live together.

- £0 to £6,000: Your ESA is not affected

- £6,001 to £16,000: Your ESA is reduced

- £16,000 or more: You are no longer entitled to income-related ESA

The DWP counts most forms of capital, including money in bank accounts, cash, Premium Bonds, ISAs, shares and investments.

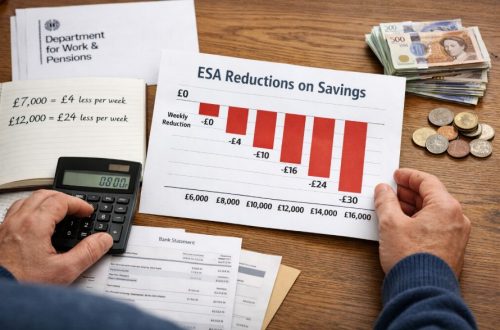

How the DWP Reduces ESA Between £6,000 and £16,000?

Once your savings go above £6,000, the DWP reduces your ESA by £1 per week for every £250, or part of £250, over the £6,000 threshold.

For example, if you have £7,000 in savings, you are £1,000 over the lower limit. The DWP divides that amount by £250, which means your ESA is reduced by £4 per week.

| Savings Amount | Amount Over £6,000 | Weekly ESA Reduction |

| £6,000 | £0 | £0 |

| £7,000 | £1,000 | £4 |

| £8,500 | £2,500 | £10 |

| £12,000 | £6,000 | £24 |

| £16,000 | £10,000 | ESA stops |

Real-Life Example of an ESA Claimant

Martin, aged 52, receives income-related ESA in the Support Group and was recently left £8,200 by a relative. He worried that he would lose all of his benefit.

After contacting Citizens Advice, he learned that his ESA would not stop immediately. Instead, because his savings were £2,200 above the £6,000 limit, his payment would be reduced by £9 per week.

Martin said:

“I thought I would lose my ESA completely, but it turned out that only a small amount was deducted each week.”

This example shows why it is important not to panic if your savings rise above £6,000. The DWP usually reduces your ESA gradually until your capital reaches £16,000.

Does New Style ESA Have a Savings Limit?

New Style ESA does not have a savings limit because it is based on your National Insurance contributions rather than your household income.

You can have any amount of savings and still receive New Style ESA, provided you meet the other conditions, such as having enough National Insurance contributions in the last two or three years.

However, New Style ESA can still be affected by private pension income. If you receive more than £85 per week from a pension, half of the amount above £85 is deducted from your ESA.

For example, if you receive £125 per week from a private pension, the DWP ignores the first £85. The remaining £40 is halved, so your ESA would be reduced by £20 per week.

“New Style ESA is based on contribution history rather than savings, but private pension income can still reduce the award,” according to Citizens Advice guidance.

This distinction is important because many people confuse pension income with savings. Having money in a savings account does not affect New Style ESA, but a regular pension payment might.

Does PIP Affect the ESA Savings Limit?

Personal Independence Payment (PIP) does not have any savings limit. You can receive PIP regardless of how much money you have in the bank.

However, PIP does not remove the savings rules for income-related ESA. If you receive both benefits, your PIP stays the same even if your ESA is reduced because of your savings.

This means:

- PIP is never reduced because of savings

- ESA may still be reduced if it is income-related

- Receiving PIP does not give you a higher ESA savings limit

Many people in the ESA Support Group also receive PIP, which can make the rules seem confusing. The important point is that the two benefits are assessed separately.

For example, if you have £12,000 in savings and receive both PIP and income-related ESA, your PIP remains unchanged. Only the ESA is reduced.

What Counts as Savings for ESA?

When assessing your ESA claim, the DWP uses the term “capital” rather than “savings”. Capital includes most money, assets or investments that you can access, whether they are held in your name alone or jointly with someone else.

The DWP usually counts the following as savings:

- Money held in current accounts and savings accounts

- Cash kept at home

- ISAs, Premium Bonds and other savings products

- Shares, investments and unit trusts

- Any property you own apart from the home you live in

- Your partner’s savings, if you live together

These forms of capital are added together to work out whether you are under the £6,000 limit, between £6,000 and £16,000, or above £16,000.

However, not every payment is treated as savings straight away. Some types of money may be ignored for a period of time. This can include backdated benefit payments, compensation awards, or money received following a tribunal decision.

In many cases, these amounts are disregarded temporarily, giving you time before they affect your ESA.

Property and Other Assets

If you own a second property, the DWP may include its value as part of your capital. This could be a house, flat or land that you do not live in. The home you normally live in is not counted.

There are some exceptions. The value of another property may be ignored for up to six months if:

- You are trying to sell it

- You intend to move into it

- You have left the property following a separation or relationship breakdown

After six months, the DWP may review the situation and decide whether the property should then be included as capital.

Partner’s Savings

If you live with a partner, the DWP looks at your finances as a household rather than individually. This means your partner’s savings are added to yours when calculating your ESA entitlement.

For example, if you have £3,000 in savings and your partner has £4,500, the DWP treats you as having total capital of £7,500. Because this is more than £6,000, your income-related ESA could be reduced.

This often catches couples by surprise, particularly if one person has little or no savings of their own. Even if the money is in your partner’s sole account, it can still affect your ESA claim if you live together.

What Happens If Your Savings Go Above the ESA Limit?

If your savings increase above £6,000, you should tell the DWP straight away. Failing to report a change could lead to an overpayment, and you may be asked to repay the money later.

If your savings reach £16,000 and you receive income-related ESA, your claim usually ends. In some cases, you may be able to claim Universal Credit instead, although different rules apply.

The DWP can also investigate how your savings were spent. If it believes you deliberately gave away money or spent it simply to keep your benefits, it may apply “deprivation of capital” rules.

For example, if someone withdrew £12,000 and gave it to a family member purely to stay below the ESA savings limit, the DWP could still treat them as having that money.

Are There Any Exceptions to the ESA Savings Rules?

Some types of capital are ignored temporarily. These exceptions can make a significant difference if you have recently received a large payment.

The DWP may ignore:

- Backdated benefit payments for a limited period

- Compensation payments in certain circumstances

- The value of a property you are trying to sell

- Money set aside for specific disability-related needs

Because these rules can be complex, it is often worth speaking to Citizens Advice or a welfare adviser if you suddenly receive a lump sum.

How Do You Check Which Type of ESA You Receive?

If you are not sure which type of ESA you get, the easiest way to find out is to read your latest award letter. It should state whether you receive:

- Income-related ESA

- Contribution-based ESA

- New Style ESA

If the letter is unclear, contact the DWP and ask them to confirm which type of ESA you are on. This is the most important step before working out whether your savings affect your benefit.

Conclusion

The ESA Support Group does not have its own separate savings limit. Instead, the amount you can save depends on the type of ESA you receive.

If you get income-related ESA:

- Up to £6,000 in savings has no effect

- Between £6,000 and £16,000 reduces your ESA

- £16,000 or more usually stops your ESA

If you get New Style ESA or contribution-based ESA, your savings do not matter at all.

Always tell the DWP if your savings increase, particularly if they go above £6,000, to avoid overpayments or problems with your claim.

Conclusion

The amount of savings you can have on ESA Support Group depends entirely on the type of ESA you receive. If you get income-related ESA, savings up to £6,000 will not affect your payments, while amounts between £6,000 and £16,000 can reduce them.

Once your savings reach £16,000, your entitlement usually ends. However, New Style and contribution-based ESA are not affected by savings.

Always check your ESA award letter and report any changes in savings to the DWP promptly.

Frequently Asked Questions

Can you stay in the ESA Support Group if your savings go over £16,000?

Yes, you can remain in the Support Group, but you will usually lose entitlement to the income-related part of ESA if your savings reach £16,000.

Do joint savings affect ESA Support Group claims?

Yes. If you live with a partner, the DWP combines both of your savings when calculating income-related ESA.

Is PIP stopped if you have more than £16,000 in savings?

No. PIP is not means-tested, so your savings do not affect it.

Does money in an ISA count as savings for ESA?

Yes. ISAs are treated as capital and count towards the ESA savings limit.

Will the DWP check if your savings increase?

The DWP can ask for bank statements or other evidence, especially if your circumstances change or your claim is reviewed.

Can ESA be reduced because of a partner’s money?

Yes. For income-related ESA, your partner’s savings and income can reduce your payment.

What is the difference between income-related ESA and New Style ESA?

Income-related ESA is means-tested and affected by savings. New Style ESA is based on National Insurance contributions and ignores savings.